What are the two types of lenders who won’t last? Those who don’t use their data.

All jokes aside, data is the lifeline that keeps lenders ahead of their challenges. There will never be a time with no struggles to overcome. The way that every financial institution has endured is by planning with data.

Who are lending metrics really for?

Smaller lenders may think they’re exempt from the rule that businesses need data. That couldn’t be farther from the truth. Small lenders significantly benefit from collecting and analyzing their lending metrics. While larger firms can weather a little more damage, others need to carefully plan each step for their success.

Some of the most valuable information likely won’t come from any one lender. Instead, compiled industry data should guide your next steps. For example, mortgage lenders should stay on top of property records and the movement of assets to make educated decisions. It can also help you steer clear of trouble. Market watching, especially during a recession, can prepare lenders for what’s to come.

The new-tech jitters?

It’s not uncommon for fear of technology to hold lenders back from capturing and utilizing their data. And reasonably so. For someone whose business is money, the idea of losing both time and money by adding tech is an absolute no. If your staff is not tech-savvy, the apprehensions grow.

That said, the tech that lenders use knows about these apprehensions. Many have full teams to handle implementing the tech and training your staff. In any case, it’s good practice to outline your concerns with your team before interviewing tech providers.

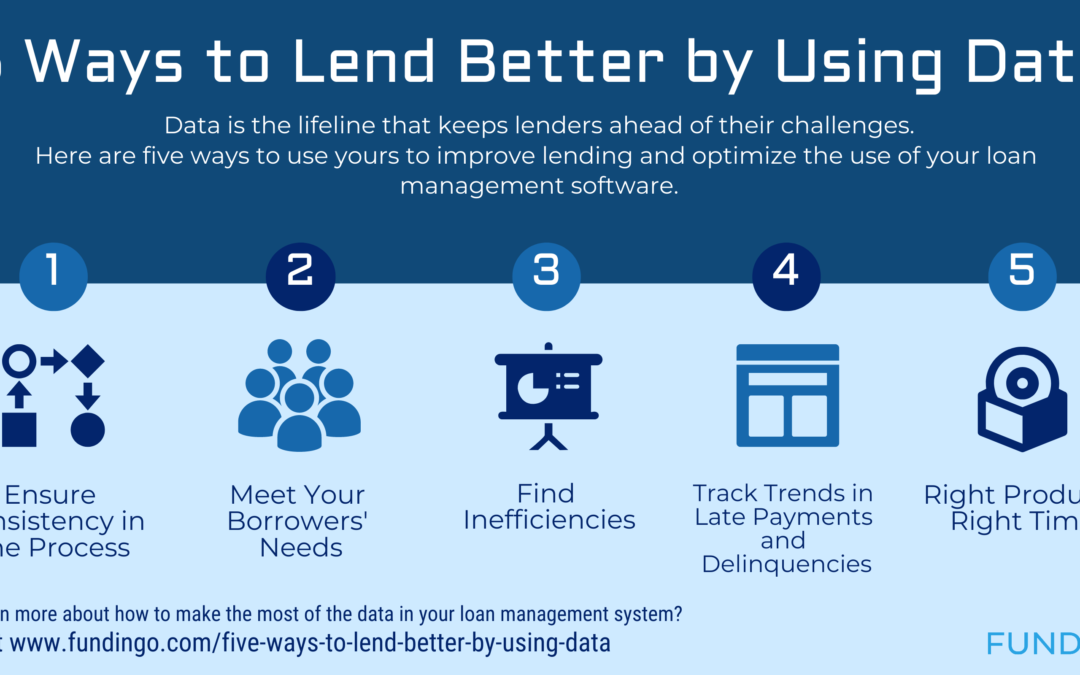

So, what are the five ways data can improve your lending

1. Ensure consistency in processes

How can you be sure you’re following the right protocol if you have nothing to check? Missing information, disorganized flows, and fragmented processes cost time and resources. However, just a little time spent organizing your process results in mountains of useful information.

First, make sure you know what you want from your data. What processes are you trying to improve? Are you already experiencing a problem or looking to enhance your existing flows? Once you have what you want, see what your current data has and lacks. To get the best insights, you’ll need high-quality data.

Some loan management software will go as far as to alert you to inconsistencies. Of course, with unified data, you can then compare deals and pull more significant insights. Every insight you get depends on the quality of your data. Make sure that it’s complete.

2. Meet your borrowers’ needs

How can you tell that you’re taking action on your deals on time? Do you have a log of communications with your customers? If you don’t, you may be missing significant opportunities to cultivate repeat deals.

Studies show that your customer experience is the number one factor clients consider when selecting software. These experiences don’t just include how they interact with your technology, but also your customer service and overall speed.

When you begin, start with a baseline assessment of your customers’ experience. For example, what are your current metrics for customer care? How are you collecting them? If you have trouble answering those questions, then think hard about the software you’re using.

Cloud lending software lets you see the detailed history of your communications with your borrowers. If one or more deals encounters an ongoing problem, you can see the email chain, messages, and actions taken to solve it. In a similar respect, this brings systemic issues to the surface, so you don’t have to spend as much time searching.

3. Find inefficiencies

Speaking of, do you know how long you spend finding those systemic issues? After ensuring your data is complete, you can then understand the amount of time spent on any given step. Digital lending apps eliminate most duplicate processes, but some may still slip past you. Take a close look and detailing your procedures using your data. Where do you see redundant, time-consuming, or unnecessary steps?

These analyses are necessary under normal circumstances but critical in financial downturns. Collecting essential data during prosperous times helps your business pull through its struggles. Knowing how to identify them early is one of the superpowers of data for lending.

And what about those wasteful processes? You can use them to identify opportunities to optimize pieces of your lending with AI or process integrations.

4. Track trends in late payments and delinquencies

Late payments happen. Delinquencies, too. But when is a one-time event really part of a bigger pattern?

Digital lending systems can highlight deals or borrowers with repeated missed payments and highlight risk factors before they go into default. Considering the challenges lenders face, looking at new risk indicators is the only way to stay afloat.

What is your company’s plan to ride out the next financial downturn? Of course, they will happen, but you must steer yourself to safety with data. By collecting data both in good times and bad, you learn where (and where not) to steer your operations.

5. Right product, right time

You may think you know your clients inside and out. How can you be sure without data? Smart, data-driven lending covers more than knowing how they work. It helps you offer them the right product at the right time for the right price.

Demographics data guides you to your customers. After all, the needs, preferences, and results that baby boomers value are undoubtedly different from younger generations. Your demographic guides you on how to structure and price your loans. Offering the right product to the right audience has the bonus of increasing originations and lowering delinquency rates.

Final thoughts

Lending without data is a lucky guess at best. Especially in uncertain times, your lending NEEDS data to survive. Keep in mind that your competitors may already be using this and more in their lending. While other factors, like your software and team, steer your company in the right direction, the only test to be sure lies within your data. Only then can you begin to prepare your lending for future trends.

Having apprehensions about technology is expected. Keep them in mind and discuss them when addressing your software and lending metrics. These apprehensions are not a barrier to your use of data but essential considerations that help you find the right fit. Remember, data is there to help you. It’s the map that leads you to your destination.

Though finance is seeing its peak of online interactions, one sector still lags. Due to a complicated history of legislation, mortgage lending has taken place primarily in person since its beginning. Now, with online finance lagging in the pandemic recovery, how far does mortgage lending have to catch up?

Consider how far the process of buying a house has come in the last 20 years. Buyers can find homes as easily online as they once could with real estate agents (and at a significantly reduced cost). They can shop for a mortgage online and see their potential rates in different areas. Legal questions can be asked and answered online, saving them time and lawyer fees. So why do they still have to complete the process of mortgage borrowing mainly in person?

If you consider the history of mortgage lending and its first steps into the digital realm, the reasons become clear. Regardless of its roots, mortgage lending must catch up with its digital siblings to stay afloat. Otherwise, like many businesses affected by the pandemic and changing demographics, it will see itself replaced by other services as well.

The Origins of Online Lending

The roots of online mortgage lending go back to the late ’90s. Its first obstacle to overcome was the process of signing documents. Historically, document signing took place in person only with no legal alternatives. This method of signing was the only option until the advent of the e-signature. Its invention, however, did not see the most comfortable start. Concerns of fraud led to uncertainty among states, snowballing into confusing (and sometimes even contradictory) legislation on a state level.

The biggest challenge with this method was the e-signature’s validity across state lines. While some states legislation was compatible, others left both signers and lenders perplexed. For instance, what if signers lived in different states? Whose state rules took precedence over the interaction? And if brought to court, would it indeed be legal? Without proper guidance, signers were reluctant to make the shift to e-signatures on their documents. Their caution and lack of federal action held back the industry from its next step forward.

Later, e-signatures were legalized throughout the US one law, called the Uniform Electronic Transactions Act. This act eliminated conflicting regulations governing each state and made online signatures uniformly legal throughout the United States. The federal ruling overrode the conflicting individual legislations and confusing fraud protections that had scared many away from digitally signing.

Digital signatures have since allowed individuals and businesses to take advantage of the convenience of online operations. Signing contracts can take place in different parts of the country without the concern of their legality. However, the movement from a hybrid to a digital lending process is not yet complete. Now that signing could take place online, the next biggest hurdle is notarization.

Current-Day Struggles

While many parts of the lending process can take place online, notarization still takes place in person. Now, online loan applications are commonplace, with millennials seeking out online experiences versus in person for convenience and safety. This change means that lenders will have to move from paper operations to digital systems to keep up with the demand. If not, they risk being replaced by lenders that will.

A shifting demographic is not the only reason for lenders to push for online mortgages. Not only does it benefit their borrowers, but it reduces effort on the lenders’ side. A report from the New York Federal Reserve concluded that the processing time for online mortgages and refinancing is significantly less than in-person or hybrid transactions. It stated that processing took an average of 14 days fewer when refinancing with online lenders versus the alternatives, and processing for purchases took 90 shorter on average.

Though hesitation is common among lenders, increased demand for funding and pressure to operate digitally strain their current practices. That said, their skepticism is not unwarranted. Even the most willing still exist in a landscape where legislation has not kept up with their new needs.

Challenging Times

Naturally, many lenders are apprehensive when considering changing from their current methods. Legislation, rigid legacy software, and the perceived difficulty of change hold back businesses from keeping up with the present. However, the reduced labor and digitalized processes will no longer be optional, but critical to their businesses’ survival.

Given the pressing financial landscape, reduced processing time is a significant benefit. More individuals are applying for mortgages and refinancing because of pandemic stress. Families now have to share spaces for even more time, with children only beginning to return to school and many colleges refusing to open dorms.

What Does the Future Hold?

Now, lending is bowing from the pressure to adapt to a new demographic and the pandemic’s urgency. The next obstacle to overcome is the struggles of digital notarizing. Though some platforms such as QuickenLoans have found ways to navigate this, the entire industry will need to adapt.

Years from the first steps leading to online mortgage lending, notarization faces similar challenges. Currently, states have a patchwork of laws, much like those that were initially governing online signatures. This dilemma raises some interesting questions. Is it legal to have a notary reside in one state & for parties living in another? Does the notary have to be in the same state as the signers? Like the case of online signatures, lenders fearing legal repercussions still find it safer to rely on physical documents to make sure that they are compliant with the law.

An Unforeseen Development

The current landscape of mortgage lending is far beyond what we would have imagined in the late ’90s. Now, a worldwide pandemic has pushed businesses either online or out of existence. Those that can adapt are those that can lend online. Many banks have based intense criticism for their lack of accommodations for their clients. Social distancing makes individuals wary of meeting in person, and hesitant lenders are sticking to the former status quo to avoid legal trouble.

Unfortunately, this puts many financial institutions at risk of falling behind. Clients are leaving their current banks for those that offer a better online experience. Even medicine has embraced telehealth to keep both doctors and patients safe. On the other end of the spectrum, finance has seen even more confusion from rushed legislation, leaving them unclear about how to comply.

The new way of life depends primarily on online interactions. Naturally, it would make sense that the remaining challenges in mortgage lending catch up with the times. In addition to the pandemic’s effect on how people go about their day-to-day life, millennials are reaching home-buying age and expect a fluid online experience. They will actively choose lenders and other services that provide a better and more coherent experience. Traditional lenders and those wary of migrating their services online despite the resources available are at risk of becoming obsolete in light of the coming change.

What’s Next in Online Mortgage Lending?

The final frontier for mortgage lenders is the legalization of digital notary services. While online mortgage lending has advanced by leaps and bounds over the last 20 years, this final obstacle between lenders and borrowers holds back a significant advance in how property purchases take place in the new normality.

The next change has to take place on a federal level. Mortgage lending, there must be one law unifying the requirements to notarize online. Following this, mortgage lending can join fintech in a wholly digital arena. While we wait for the legislation to come, prepare your staff and operations to embrace digital lending. When both businesses and individuals need more financial assistance than ever, lending must be there to give a helping hand.

For the first time in history, the value of oil dropped into the negatives in April. While it has recovered for now, some are predicting an incomplete recovery at best. In the greater context of post-COVID life, the safest investments will be green.

Construction has faced numerous challenges since the beginning of the pandemic. Supply-chain interruptions and rising costs of materials posed a unique set of issues to the industry. While new construction has ultimately slowed, the industry remains surprisingly resilient despite the struggles. Now, buildings are being designed for the next 100-year flu and a greener future overall.

What is driving the uptick in green construction? For one, it’s less risky overall. With uncertainty regarding fossil fuels, heating, air conditioning, and ventilation will have to become more efficient. Now that the virus’s spread is proven to increase in poorly ventilated areas, builders will have to rethink the tightly sealed construction that once made air conditioning more efficient.

Why Green?

For a safe return to the office, traditional construction will no longer make the grade. Not surprisingly, lenders are increasingly wary of offering to fund projects that cannot weather an uncertain future. Naturally, given the risk, both builders and lenders are looking towards the future through green-colored glasses.

Green construction companies are also on the rise. According to a report from The U.S. Green Building Council and Dodge Data & Analytics, 45% of those surveyed expected most of their projects by 2021 to be green construction. Given the additional push of the pandemic, those numbers could now be even higher.

New construction isn’t the only focus either. A significant amount of construction projects will include retrofitting older buildings with more environmentally-friendly fixtures. According to the same report, changes such as these will lead to a 13% decrease in operating costs over five years.

Lenders have been even warier of risk since the pandemic. In order to continue, they need to focus on construction that will be resilient during any future changes. Things will certainly not go back to how they were, but instead of lamenting, lenders must embrace the changes to continue moving forward.

To learn more about how Fundingo helps construction lenders adapt to the new dynamics of the pandemic, click here.

According to Zillow, new work-from-home jobs could result in nearly 2 million potential home-buyers. According to the study, “Three-quarters of Americans working from home because of the coronavirus say they want to continue if given the option, and two-thirds say they would consider moving if given that flexibility.”

Before the pandemic, house options were tied to job locations. Distance work now offers them options in new areas. The study focused on renters earning wages too low to buy a home where they currently live. They then considered if their wages were high enough to buy one elsewhere. Millennials make up nearly half of that two million that fit those criteria. They expressed more interest in living in suburban or rural areas than older generations.

Education will play a key role in helping these people become home-buyers. Many do not know of the incentives for purchasing homes in rural areas, or those for low-income families. By finding individuals when they start to consider buying a home, lenders help them become well-prepared mortgage borrowers.

Now what?

To find these individuals, lenders must know where to look. Almost half of the two million potential buyers will be between 26 and 40, and very tech savvy. They use primarily online tools to search for homes and mortgages.

To see things from their perspective, lenders must evaluate their lending processes from the borrower’s perspective. How is their online experience? What still takes place in person? Does the lender keep their data organized or spread across multiple programs?

If there are any faults in the process, consider what can be done to make it more approachable. See where online customer service, including chat functions and blog resources, can expand. There is a wealth of software available to lenders to keep processes organized—this stores data on applications and borrowers in one place.

By analyzing processes now, lenders will be in the right position to capture the wave of borrowers when they begin looking. When jobs finally announce permanent work-from-home opportunities, online resources should guide new incoming borrowers to lenders’ applications. Changing to keep up means things have already fallen behind, so remember to always change to stay ahead.

The pressure to find new homes during the pandemic does not come as a surprise. With mandatory lockdowns, individuals and families are finding themselves behind closed doors more than ever before. Schools and universities are delaying or even cancelling in-person classes. Space is tight, stress is high, and naturally, people are seeking new opportunities to be comfortable in their space.

Following this push, sales of new homes have reached a 13-year high. Naturally, wealthy individuals are the vast majority of current home-buyers, with renters still reeling from the hit. Low-income and middle-class families are struggling more than ever to continue paying their rent. Additionally, protections against eviction and unemployment benefits have been cut and house prices are shooting up.

Coupled with the increase in new home sales, sales on existing homes have remained steady as well. Even purchases of homes that haven’t begun construction have seen a 34% year to year leap. Low interest rates coupled with the pressure of distancing and lockdowns have opened up a new opportunity for lenders to aid buyers in their search.

Mortgage application rates have soared as well, but many lenders relying on manual processes may struggle to keep ahead of the boom in home purchases. Those with lower-quality customer service and in-person operations are already falling behind as customer expectations continue to set the new standards for lending.

Will your business be able to keep up with the rush? Schedule a consultation to find out where your weakest points are and how you can stay afloat.